The famous quote of George Santayana, “Those who cannot remember the past are condemned to repeat it.” With the objective of learning from the past, we will revisit some of the classic legal judgments, deliberations, and decisions, and link them to present situations. In public life, decisions taken decades ago by courts, legislatures, and regulators continue to remain relevant for years together. The context may have faded, but their lessons stand the test of time. Echoes of the Past and Lessons for the Present seeks to revisit such defining episodes. These are not merely the stories of the past; they are living examples that continue to inform how we think about accountability, public institutions, and the exercise of government power.

Life Insurance Corporation: A Young Institution in Crisis

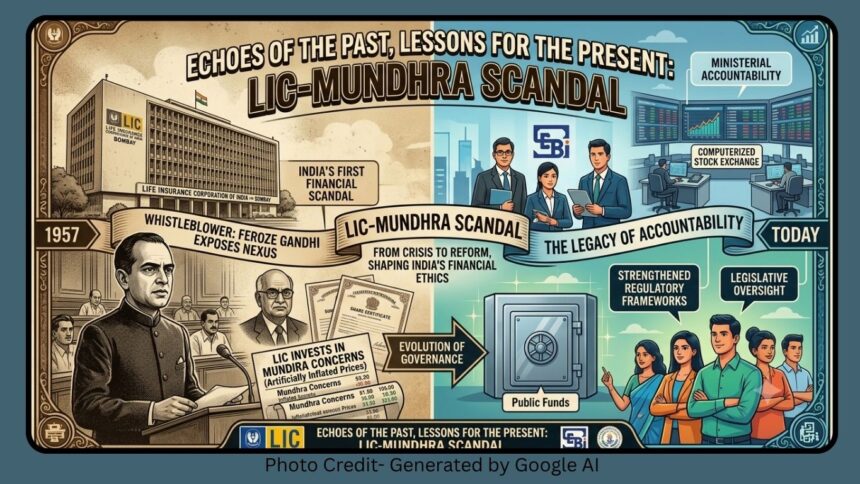

In this article, we turn to one of the earliest and a high profile financial controversies of Independent India: the LIC–Mundhra case, that rocked the parliament in 1957. It is a path-breaking case that established principles of public accountability, institutional integrity, and government responsibility that continue to echo even today.

The Life Insurance Corporation of India (LIC) was established in 1956 and was entrusted with the responsibility of managing the savings of millions of Indians. LIC was expected to work as a custodian of public money. It was a living manifestation of public trust. Within one year of its existence, it came under public scanner for its investment in the companies owned by Mr. Haridas Mundhra. Those companies were financially weak, and their shares were widely regarded as speculative and unsound.

LIC was forced to buy shares worth over Rs 1.26 crore of Mundhra companies at a price higher than the market price in a private transaction. Moreover, it was observed that the transaction happened on a day when both the Bombay and the Calcutta Stock Exchanges were closed.

The Whistleblowers: Parliamentarians from the Treasury Bench

Two MPs from the treasury benches, Dr Ram Subhag Singh and Mr Feroze Gandhi, raised questions on the basis of The Statesman’s report dated 3 August 1957 about LIC’s investments in Mundhra’s companies. Their intervention transformed the case from a routine financial anomaly into a political crisis.

The then Finance Minister, T. T. Krishnamachari (TTK), conceded that LIC had invested in firms owned by Mundhra. However, he claimed that all investment decisions were taken by an LIC investment committee, and that the government had no role to play. The MPs, however, continued to question the propriety of the investment and demanded accountability by sharing all details with the people of India.

The Investigation Process: Unprecedented Transparency

The Government of India appointed a one-man judicial inquiry Commission headed by the Chief Justice of the Bombay High Court, M. C. Chagla, on 7 January 1958. The Commission marked a turning point in India’s approach to public accountability. Justice Chagla insisted on transparency right from the beginning. Hearings were conducted in public, allowing citizens and the press to witness how accountability was established in real time. It signaled that matters involving public funds must be subject to public scrutiny.

The Commission completed its investigation in 25 days and submitted a detailed report. The Commission established that LIC’s investment in Mundhra’s companies was unwise and unjustified. The normal decision-making channels within LIC had been bypassed. More significantly, it concluded that there had been undue influence from the Finance Ministry in pushing through the transaction.

Justice Chagla stressed that LIC’s resources represented the collective savings of citizens. Using such funds to support failing private enterprises raised serious economic and ethical concerns. The Commission said in its report: “It would be clearly wrong for the Corporation (LIC) to utilize its funds to help an individual or the concerns of an individual. It would be even worse for the Corporation to deal with an individual who was suspected to be a lawbreaker and possessed a doubtful financial reputation and whose antecedents were of a most questionable character.”

He also highlighted the erosion of institutional processes. Institutions derive their strength from rules, checks, and internal control mechanisms. Evading these processes in such an important decision was not in the larger interest of the organization and its stakeholders.

Justice Chagla in his report underscored the importance of ministerial responsibility. He noted that, constitutionally, the minister was responsible for the actions of his secretary with regard to the LIC transactions. He said, “It is clear that the minister must take responsibility for actions done by his subordinates. He cannot take shelter behind them, nor can he disown his actions.”

The Consequences

Following the Chagla Commission’s report, TTK submitted his resignation on 18 February 1958. His resignation was not merely a political act; it was a reiteration that ministers are accountable for the actions of their departments. The Finance Ministry’s Principal Secretary, H. M. Patel, and LIC Chairperson, K. R. Kamath, also resigned.

Haridas Mundhra was arrested and eventually convicted. This demonstrated that private actors who benefited from questionable state actions would not remain beyond the reach of the law.

The case strengthened parliamentary oversight over public financial institutions. It reinforced the expectation that entities like LIC must function with utmost professionalism.

The Echo: The Judgment Is Still Relevant

With the passage of time, every crisis ends, and people may even forget the crisis. But some leave a lasting legacy. More than six decades later, the LIC–Mundhra scandal continues to echo in the corridors of power and the corporate world. Its relevance lies not in its historical novelty, but in the observations and judgements of the Chagla Commission.

The first concerns the stewardship of public money. Today, institutions such as LIC, public sector banks, and sovereign funds manage vast pools of capital. The scale may have changed, but the principle remains the same: these funds belong to the public, and their investment must adhere to prudent and transparent policies. As per several reports, LIC’s investments in the shares of Adani Group companies are around Rs 39,000 crore, and in the recent past, LIC subscribed to the entire ₹5,000-crore non-convertible debenture (NCD) issue of Adani Ports. The Indian Express reported that LIC increased its stake sharply in four of the seven listed Adani Group companies over just eight quarters since September 2020.

However, there has been little discussion about the basis of the investments. The common shareholder can only hope that the principles of Justice M. C. Chagla have not been violated. One also hopes that these investment decisions were guided not only by conventional financial metrics but also by integrity in the process.

The case also demonstrated the proactive role of parliamentarians highlighting the importance of parliamentary vigilance. One hopes that present parliamentarians and other office bearers of constitutional bodies maintain such a high level of integrity and accountability.

In the Gandhian spirit, there is no such thing as ‘away from the public eye’ in matters of public trust. One hopes that today’s custodians of public money adhere to these principles, as echoed in the judgement of Justice M.C. Chagla.

Prof. D. V Ramana traches at Xavier Institute of Management University, Bhubaneswar. He writes regularly for different news publications and web papers.

Prof. D. V Ramana traches at Xavier Institute of Management University, Bhubaneswar. He writes regularly for different news publications and web papers.

Comments

0 comments